Case Study

651.56% backtested return

from a 72H Z-score Bitcoin strategy

Overview

We asked our AI to identify datasets correlated with BTC’s future price.

It found several, with one showed a 0.67 correlation. From that dataset, our AI

engineered features and ran a backtest with defined cost assumptions and

basic risk controls to evaluate trading performance.

Trading Strategy

The base trading strategy testing was designed around entry and exit rules

using Z-score signals specific lookback window, with a short holding period

to manage exposure and cost.

Assets

BTC

Signal Filtering

Only certain % of Z-score signals were used, selected by our AI Data Science signals.

Transaction Cost

0.025%

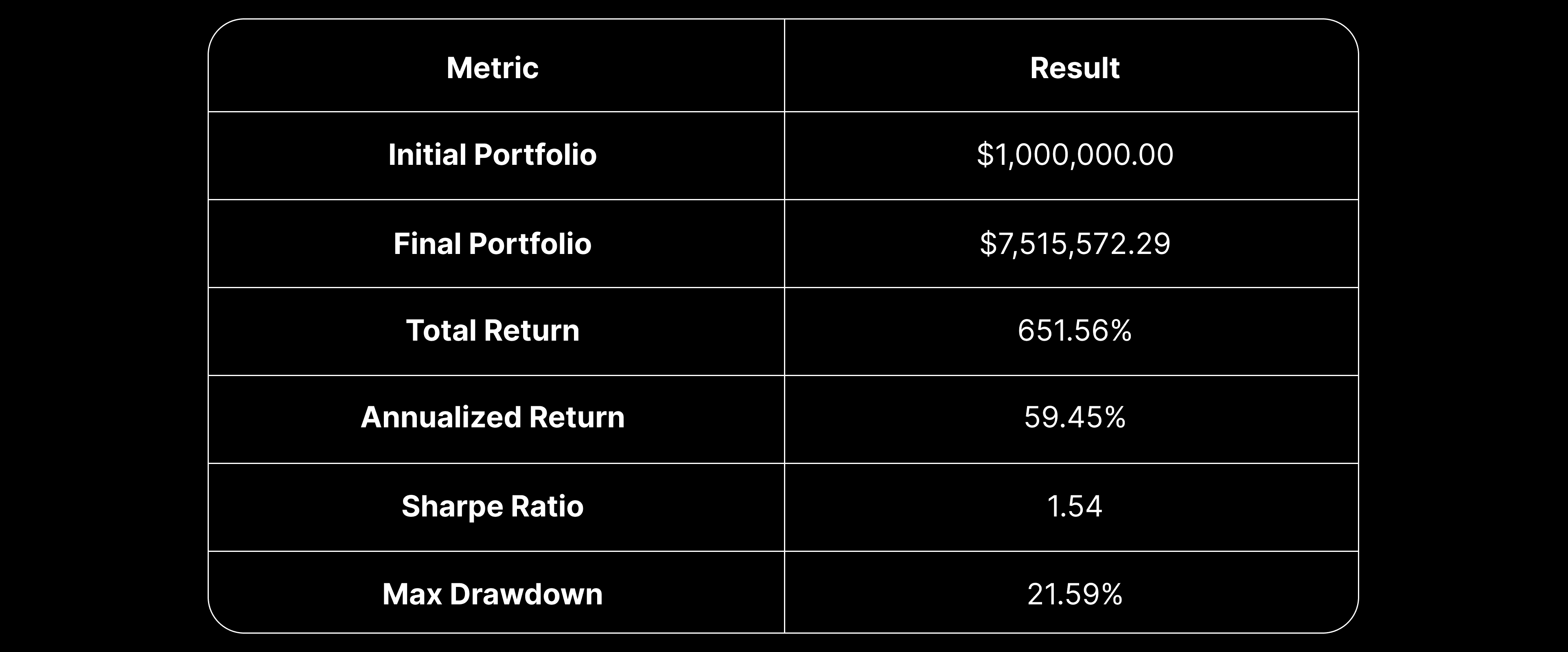

Performance Summary

Backtest Period

Jan 3, 2018 — May 24, 2025 (2,697 days)

Why This Matters

Our strategy outperformed many BTC benchmarks using clear entry and

exit rules, short holding periods, and cost assumptions. The backtest highlights consistent performance in terms of returns, drawdowns, and trade behavior.

We added Monte Carlo simulations to understand the range of possible outcomes rather than a single equity curve. By simulating thousands of P&L paths,

we could estimate the probability of adverse outcomes.

Walk-forward testing showed that the model holds up across different

market regimes including bull, bear, and sideways periods. By retraining and validating on rolling windows, we confirmed the strategy's adaptability over time.

Want a tailored strategy?

Let’s Talk

Your Data Science Team

Automated for Alpha

This information is for informational purposes only

and should not be considered investment advice.

Past performance does not guarantee future results.

Investing involves risks, and results may vary.

Strategies and performance provided are

generated by AI-driven algorithms.

© CL1CK 2025